Table Of Content

The 30-year period is your “loan term,” and usually gives you the lowest monthly payment compared to shorter terms. You may lock the mortgage rate after you have been approved and up until a few days before the scheduled closing date. As far as timing goes, forecasting rates accurately is impossible. It's best to lock when you are comfortable that you can afford the monthly payments at that interest rate.

How we make money

The details of this estimate requires some additional assistance from one of our loan specialists. Please contact us in order to discuss the specifics of your loan. However, record-low rates were largely dependent on accommodating, Covid-era policies from the Federal Reserve. And the more U.S. and world economies recover from their Covid slump, the higher interest rates are likely to go. Let’s look at a few examples to show how rates often buck conventional wisdom and move in unexpected ways.

Today’s rates for specific kinds of mortgages

Compare today’s mortgage interest rates – April 25, 2024 - CNN Underscored

Compare today’s mortgage interest rates – April 25, 2024.

Posted: Thu, 25 Apr 2024 12:25:06 GMT [source]

According to Freddie Mac’s records, the average 30-year rate jumped from 3.22% in January to a high of 7.08% at the end of October. Mortgage interest rates fell to historic lows in 2020 and 2021 during the Covid pandemic. Emergency actions by the Federal Reserve helped push mortgage rates below 3% and kept them there. Here are the factors that influence the average rates on home loans. A 5/1 ARM has an average rate of 6.89%, a climb of 10 basis points from seven days ago.

You’re our first priority.Every time.

But getting the right mortgage for your situation is also important. We focus first on understanding you and your goals, not just your finances. "This was my first real mortgage … the interest rate was way better than anyone else could offer and the process … was so fluid." The final real estate brokerage involved in a major lawsuit over agent commissions has agreed to a settlement in the landmark case.

The average rate for a 15-year, fixed mortgage is 6.76%, which is an increase of 12 basis points from seven days ago. Though you’ll have a bigger monthly payment than a 30-year fixed mortgage, a 15-year loan usually comes with a lower interest rate, allowing you to pay less interest in the long run and pay off your mortgage sooner. The rate and monthly payments displayed in this section are for informational purposes only.

What is the average personal loan interest rate?

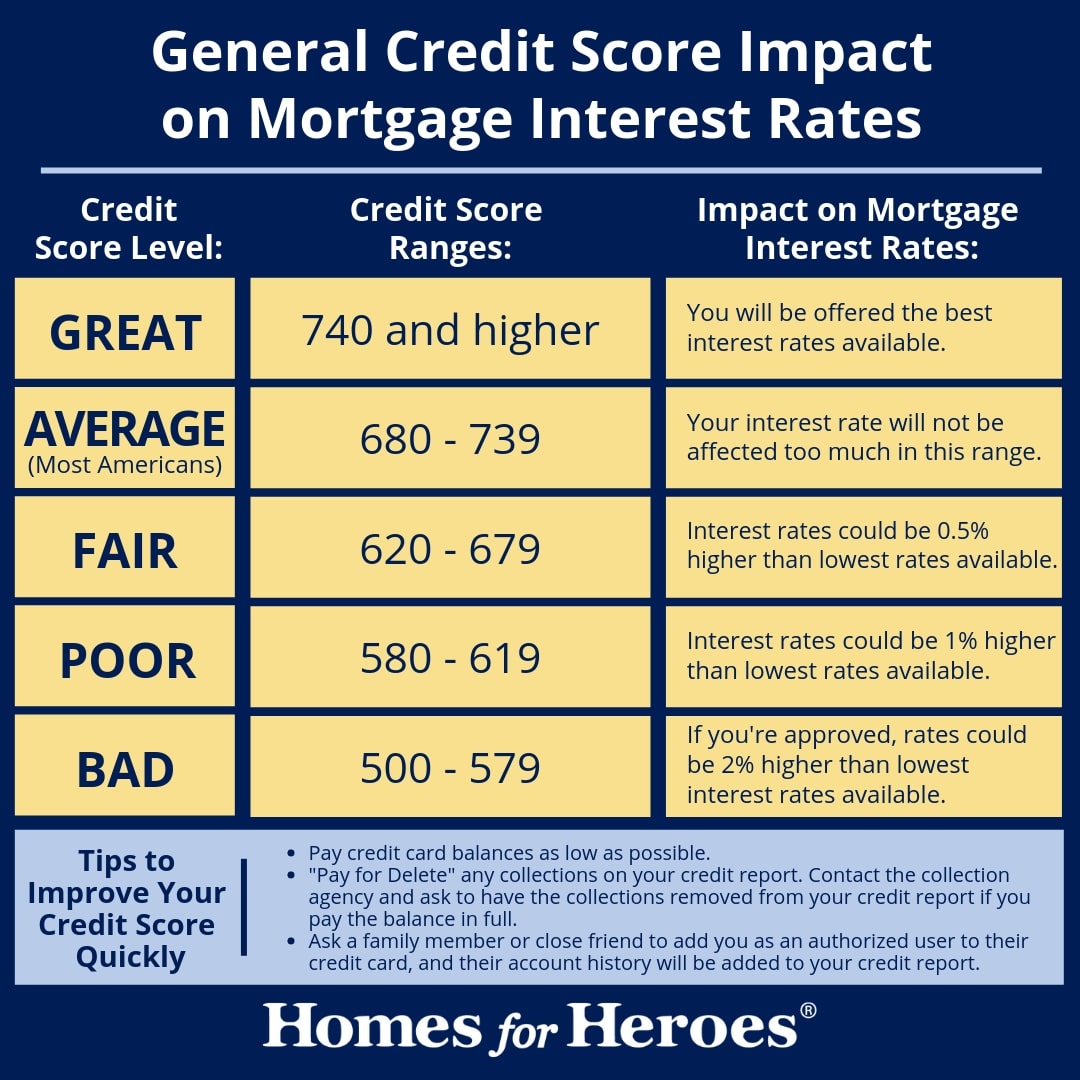

Applying for a mortgage on your own is straightforward and most lenders offer online applications, so you don’t have to drive to an office or branch location. Additionally, applying for multiple mortgages in a short period of time won’t show up on your credit report as it’s usually counted as one query. Finally, your individual credit profile also affects the mortgage rate you qualify for.

National mortgage rates edged higher for all types of loans compared to a week ago, according to data compiled by Bankrate. Rates for 30-year fixed, 15-year fixed, 5/1 ARMs and jumbo loans jumped. While the policymaker doesn't directly set mortgage rates, its decisions do influence their direction. Fixed mortgage rates move with the 10-year Treasury yield, while adjustable-rate loans more closely follow the Fed. Average personal loan interest rates can vary depending on your credit score and other factors, but you do have some control. Make sure to keep your credit score in the best shape possible and work on paying off debt to lower your debt-to-income ratio.

While the broader trends provide valuable context, it’s important to recognize that average mortgage rates are just a benchmark. Borrowers with healthy credit profiles and strong finances often get mortgage rates well below the industry norm. While it’s important to monitor mortgage rates if you’re shopping for a home, remember that no one has a crystal ball. It’s impossible to time the mortgage market, and rates will always have some level of volatility because so many factors are at play.

That's rich: Rise in all-cash transactions helping drive price gains for most expensive US homes

Our editorial team does not receive direct compensation from advertisers. It may sound like a hassle but it could save you tens of thousands of dollars. Lenders look at your debt-to-income (DTI) ratio, which compares your gross monthly income to your debts, to determine how much you can afford. Lenders usually consider a DTI ratio under 35% to be “good,” but you may qualify for a loan even with a higher DTI. Most loan programs allow for a maximum DTI ratio between 41% and 45%.

FHA loans have low interest rates, but come with mortgage insurance no matter how much money you put down. As the year concluded, the average mortgage rate went from 2.96% in 2021 to 5.34% in 2022. Although, if the Fed gets inflation in check or the U.S. enters a meaningful recession, mortgage rates could come back down somewhat.

Homeowners need to shop around to look for the best mortgage deal possible. Unfortunately, although the home is the most important asset and the mortgage is the most important liability for most households, research has shown that homebuyers do not do enough shopping. Comparing rates and fees from several lenders is important, not only from traditional lenders such as local banks, but also Fintech lenders. Importantly, when comparing offers, homebuyers need to take into account other costs beyond principal and interest payments. Federal Reserve raises its interest rate target for overnight lending between banks, and interest rates throughout the financial sector typically follow suit. From March 2022 to July 2023, the Fed raised its policy rate 11 times, leading to a surge in mortgage rates.

Limited housing inventory and low wage growth are also contributing to the affordability crisis and keeping mortgage demand down. Mortgage closing costs usually range anywhere from 2% to 6% of your total home loan amount. The cost can vary depending on many factors, including your lender and how much you’re borrowing. It’s possible to get the seller or lender to pay a portion or all of these costs.

If your details closely match those used to calculate today’s rates, possibly. Compare your credit score, debt-to-income ratio and loan amount to the ones we used by selecting the View Legal Disclosures link under where rates are displayed. The closer your details are to assumptions – you have the same credit score, the same DTI, the same loan amount – the more likely it is you’ll get a similar rate. Your rate will be different depending on your credit score and other details. Let us estimate your rate and help you reach your financial goals.

No comments:

Post a Comment